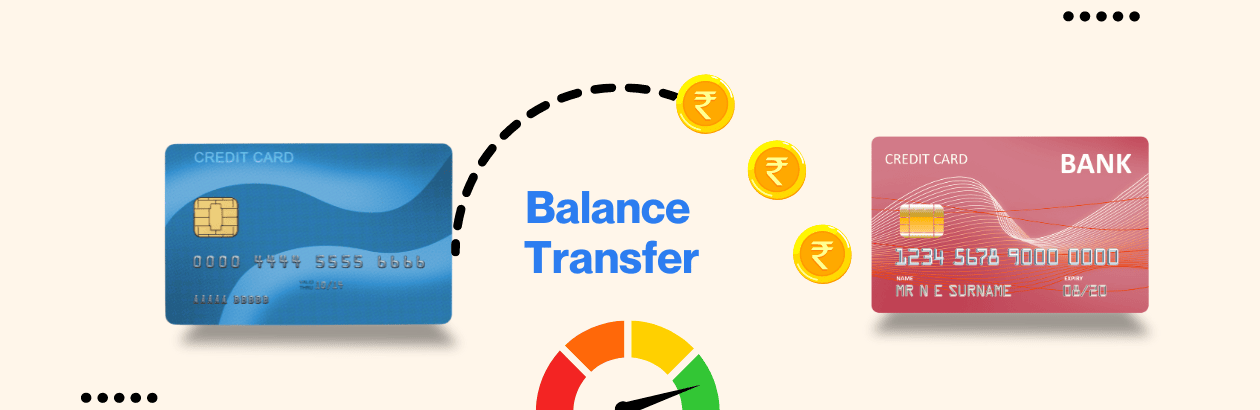

What is a Credit Card Balance Transfer?

Author And Publisher: Gyro 3.oCredit Card Balance Transfer in India

CashOn.Cards — Credit Card Bill Financing

Financial Expert Advice

Choose Your First (or Next) Credit Card Wisely

Maintain Two Credit Cards: One For Routine Expenses And Auto-Debits, And Another Reserved For Emergencies. Avoid Pursuing Rewards; Prioritize Financial Stability And Discipline.

introduction

When you have outstanding balances on a credit card and are not able to pay it in full, you may opt for balance transfer facility on other bank’s credit card. Through balance transfer, banks/NBFCs allow you to transfer outstanding balances from other bank’s credit cards and save on the finance charges and other penalties. They may also offer 0% interest rates for a limited period or other deals on credit card balance transfer. Here is all you need to know about this feature.

Key Highlights of Credit Card Balance Transfer

- Credit Card Balance Transfer helps ease the financial burden

- Transfer your balances and save on finance charges and late fee

- Consolidate multiple credit card debts into one

- 0% interest rate may also be offered for a limited period

- Stabilize and improve Credit Score

What is a Credit Card Balance Transfer?

A Credit Card Balance Transfer allows you to move your outstanding balance from one credit card to another, usually to a card with a lower or zero interest rate. This helps you save on high interest charges and repay your dues more easily.

For example, if you have Rs. 50,000 pending on a card with a high interest rate, you can transfer it to another card with a lower interest rate, which gives you some breathing space to pay it off without incurring extra costs. However, please note that such offers often come with a processing fee. It is also advisable to stop making new purchases on the new card until you clear the transferred balance.

How Credit Card Balance Transfer Works

Benefits of Credit Card Balance Transfer

Reduced Financial Strain – Balance transfer credit cards charge a significantly lower interest rate when compared to finance charges. Credit card finance charges (interest rates) are about 3.5% p.m. while the interest rate on a balance transfer is usually around 1.8% per month. Some card providers may also offer 0% interest rate. Lower interest rate means lower financial burden.

Stabilize Credit Score – Lowered interest rates will make it easier for the cardholders to make payment and hence stabilize their credit score. They can even improve it with timely payments.

Interest-Free Period – Credit card providers offer an interest-free period on new purchases post balance transfer as well. This way customer can make new purchases without incurring interest rate on it.

Other Benefits – Credit card providers sometimes offer teaser rates or other introductory offers to customers. These benefits may include longer interest-free periods, low interest rates, etc.

Pros & Cons of Credit Card Balance Transfer

Balance Transfer Pros

Helps you save on high interest charges by transferring balance to low/0% interest card.

Makes debt repayment easier by consolidating multiple balances into one.

Improves credit score if payments are made on time.

Offers short-term interest-free period for financial relief.

Balance Transfer Cons

Comes with processing fees usually 1-3% of the transferred amount.

May tempt you to overspend using the new card limit.

Missing payments or overusing the limit can negatively impact your credit score.

Not everyone qualifies for balance transfer offers due to credit score requirements.

Fees & Interest on Balance Transfer Credit Card

Processing Fee – Customers will be charged a processing fee for a balance transfer that can range anywhere between 1% and 3%. Some banks may also charge a flat fee.

Interest Rate – The interest charged on Balance Transfer can be 0% for a certain period. But, the interest rate is usually around 0.75% and may go up to the particular credit card’s finance charge.

The interest rates and processing fee charged on some popular credit card issuers are shown in the table below:

HDFC Bank Details

Shared at the time of application: 1% of BT amount, min Rs. 250

ICICI Bank Details

Starts from 2% of application: 1.5% of BT min Rs. 250

Shared at time of application

Kotak Bank Details

0% interest available

Rest shared at time of application: Rs. 349 for 6 months option

0.99% for 3 months per Rs. 10k BT amount

RBL Bank Details

Starts from 1.75% p.a.

0.99% for 6 months & Rs. 750 for option

SBI Card Details

0% interest option available, starts from 9% p.a.

NIL processing for certain plans

Rest shared at application time

Who Should Apply for Credit Card Balance Transfer?

Cardholders who are carrying significant amounts of debt at a high interest rate may apply for a balance transfer. This will help them pay off the debts without incurring hefty charges.

Do note that balance transfer is best suited when the user can pay off the due amount within a few months. If he finds that it will take longer than a few months, perhaps a year or two, then a Personal Loan will be better suited.

How to Apply for Credit Card Balance Transfer

Cardholders can apply for the credit card balance transfer via Netbanking, contacting customer care, through SMS, etc.

However, those who want to apply for a new balance transfer credit card must meet the eligibility criteria set by the particular bank for that particular card variant. Proof of identity, address and income will also be required at the time of new credit card application.

FAQ'S

Gyro - Your Financial Compass Is A Constantly Updating Financial Insights Engine That Aggregates Data From Various Sources To Provide Up-To-Date insights On Banking Products. Cashon.cards Offers Blogs, Videos, And Podcasts To Help Users Make Informed Financial Decisions.